Over half of all American farms now rely on some form of equipment financing to keep up with modern agricultural demands. With machinery costs climbing every year, many American farmers face tough choices just to maintain their productivity. Understanding how equipment financing works can give you a real edge, making it possible to acquire the latest tools while managing your cash flow and reducing financial pressure. This guide breaks down the essentials and offers clear paths to smarter decisions.

Table of Contents

- What Equipment Financing Means For Agriculture

- Types Of Equipment Financing Options Available

- How The Equipment Financing Process Works

- Key Costs, Terms, And Approval Requirements

- Risks, Pitfalls, And Common Mistakes

Key Takeaways

| Point | Details |

|---|---|

| Equipment Financing Benefits | Equipment financing allows farmers to acquire essential machinery without significant upfront costs, preserving working capital for operational needs. |

| Types of Financing Options | Common financing options include equipment loans, leasing, manufacturer financing, and agricultural credit lines, each with unique advantages and conditions. |

| Approval Process Essentials | Farmers must prepare thorough financial documentation and consider factors like credit score and projected income to qualify for financing. |

| Key Risks to Consider | Farmers should assess total ownership costs, contractual obligations, and potential technology obsolescence to mitigate financial risks in equipment financing. |

What Equipment Financing Means for Agriculture

Equipment financing represents a critical financial strategy that enables farmers to acquire essential machinery without requiring substantial upfront capital investment. Financing mechanisms play a pivotal role in agricultural productivity, allowing farmers to access modern technologies that can dramatically transform operational capabilities.

At its core, equipment financing provides agricultural professionals multiple pathways to obtain tractors, harvesters, irrigation systems, and other critical machinery through structured financial arrangements. These options typically include equipment loans, leasing programs, and specialized agricultural credit lines that distribute the equipment’s cost over manageable monthly payments. By spreading financial commitments across multiple years, farmers can preserve working capital while simultaneously upgrading their technological infrastructure.

The strategic advantages of equipment financing extend beyond immediate acquisition. Farm fleet management strategies become more sophisticated when farmers can selectively invest in high-performance equipment without exhausting cash reserves. Modern financing structures often incorporate flexible terms that account for seasonal agricultural income fluctuations, allowing farmers to align equipment payments with harvest revenue cycles.

Understanding equipment financing requires careful evaluation of several key factors, including interest rates, loan duration, potential tax implications, and the specific equipment’s projected operational lifespan. Farmers must conduct thorough cost-benefit analyses to determine whether financing represents a more advantageous approach compared to outright purchasing or equipment rental.

Pro Tip: Financial Strategy Check: Consult with an agricultural finance specialist who understands your specific farming context before committing to any equipment financing arrangement, ensuring the terms align precisely with your operational needs and long-term business goals.

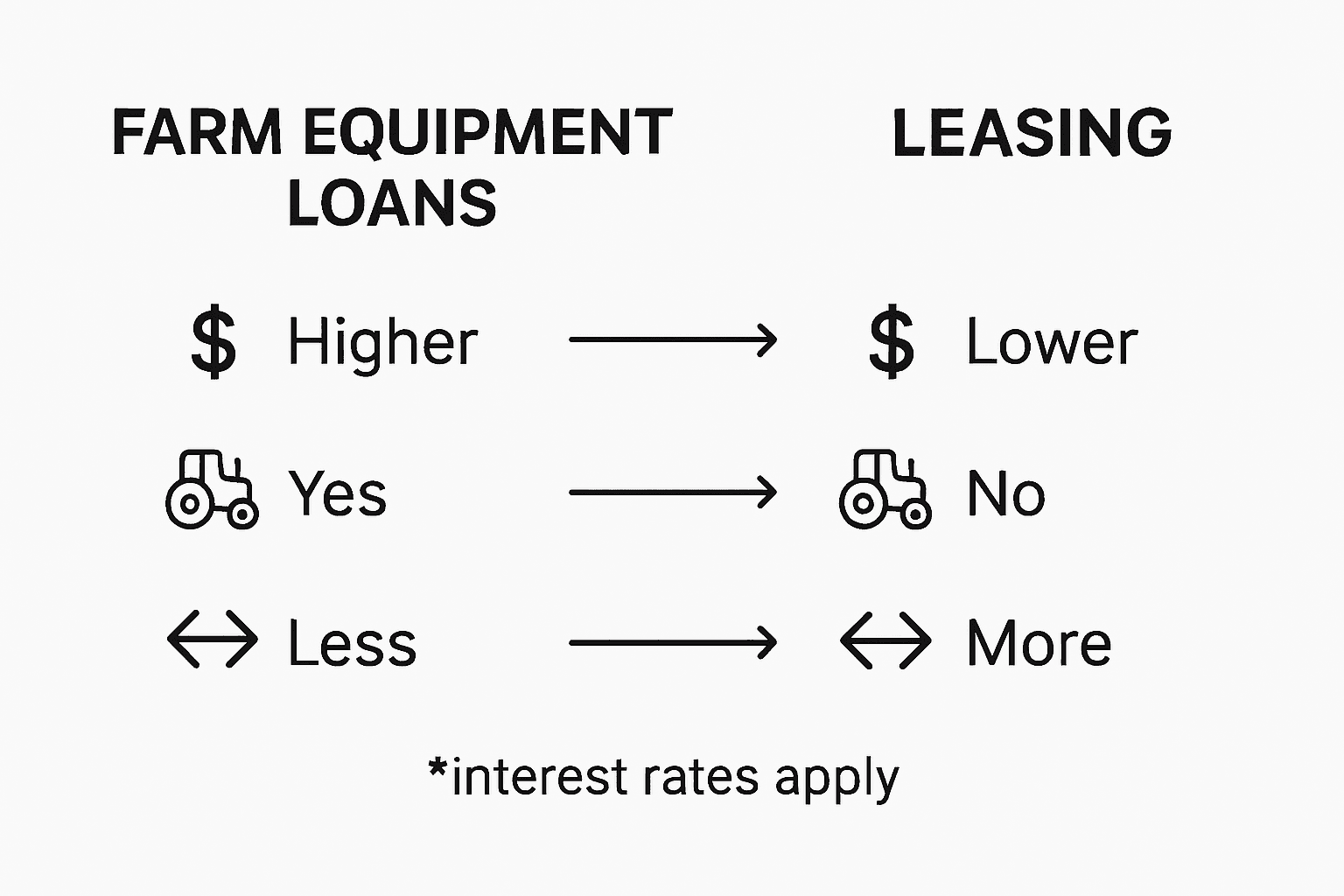

Types of Equipment Financing Options Available

Agricultural equipment financing encompasses multiple strategic approaches that enable farmers to acquire critical machinery without substantial immediate financial burden. Equipment financing options provide diverse pathways for farmers seeking to modernize their operational capabilities while managing financial constraints.

The primary equipment financing options typically include four key strategies: equipment loans, equipment leasing, manufacturer financing programs, and agricultural credit lines. Equipment loans involve borrowing a specific amount to purchase machinery outright, with farmers making consistent monthly payments over a predetermined period. These loans often feature fixed interest rates and allow complete ownership of the equipment upon final payment. Equipment leasing offers an alternative approach, permitting farmers to use machinery for a set duration without permanent ownership, which can be particularly advantageous for equipment with rapid technological obsolescence.

Agricultural equipment financing strategies also include specialized programs from equipment manufacturers and dealers. These tailored financing arrangements frequently provide more flexible terms, lower initial costs, and sometimes incorporate maintenance packages or upgrade options. Manufacturer financing can be especially attractive for newer equipment models, offering competitive interest rates and streamlined approval processes that traditional banking institutions might not match.

When evaluating financing options, farmers must carefully assess several critical factors: interest rates, loan duration, down payment requirements, potential tax implications, and the specific equipment’s projected operational lifespan. Each financing method presents unique advantages and potential limitations, necessitating a comprehensive analysis of individual farm requirements, budget constraints, and long-term strategic goals.

Here’s a concise comparison of common agricultural equipment financing methods and their distinctive features:

| Financing Method | Ownership at End | Typical Term Length | Flexibility for Upgrades |

|---|---|---|---|

| Equipment Loan | Full ownership | 3-7 years | Limited |

| Equipment Lease | No/Optional buyout | 1-5 years | High (easy replacement) |

| Manufacturer Financing | Full or partial | 2-6 years | Moderate (brand incentives) |

| Agricultural Credit Line | Varies | Continuous/renewable | Depends on structure |

Pro Tip: Financing Comparison Strategy: Collect quotes from at least three different financing sources, including manufacturer programs, local banks, and agricultural credit institutions, to comprehensively compare terms and identify the most advantageous equipment financing arrangement for your specific agricultural operation.

How the Equipment Financing Process Works

Equipment financing involves a systematic process designed to help farmers acquire necessary machinery with minimal financial strain. The journey begins with comprehensive research and equipment selection, where farmers identify specific machinery that aligns with their operational requirements and long-term agricultural strategies.

The financing application process typically encompasses several critical stages. Farmers must first gather comprehensive documentation, including business financial statements, tax returns, equipment specifications, and detailed farm operational plans. Credit evaluation represents the most significant phase, where lenders meticulously assess the farmer’s financial health, credit history, existing debt obligations, and potential revenue projections. Lenders analyze factors such as farm income stability, equipment’s potential productivity, and the borrower’s ability to generate sufficient revenue to support monthly payments.

Agricultural equipment financing strategies often involve multiple approval pathways, including traditional bank loans, manufacturer financing programs, and specialized agricultural lending institutions. Upon successful credit evaluation, farmers receive a comprehensive financing proposal detailing interest rates, repayment terms, down payment requirements, and any associated fees. These proposals frequently include options for fixed or variable interest rates, varying loan durations, and potential early payoff incentives.

Once financing is approved, the final stage involves executing the formal agreement, transferring equipment ownership or establishing leasing terms, and initiating the first payment cycle. Farmers must carefully review all contractual details, understanding potential penalties for late payments, maintenance responsibilities, and any clauses related to equipment replacement or upgrades. Some financing arrangements might include additional provisions for equipment insurance, maintenance support, or technology upgrade pathways.

Pro Tip: Documentation Preparation Strategy: Compile a comprehensive financial portfolio before applying, including three years of tax returns, detailed farm income statements, equipment specifications, and a clear business plan demonstrating how the new equipment will enhance operational efficiency and revenue generation.

Key Costs, Terms, and Approval Requirements

Equipment financing involves a complex array of financial considerations that farmers must carefully navigate to secure optimal machinery funding. The financial landscape encompasses multiple components, including interest rates, upfront costs, and comprehensive evaluation criteria that determine financing accessibility and terms.

The cost structure of equipment financing typically includes several critical elements. Interest rates can range from 4% to 25%, depending on the farmer’s credit profile, equipment type, and chosen financing method. Down payments often fluctuate between 10% and 25% of the total equipment value, with some specialized agricultural lending programs offering more flexible initial investment requirements. Additional costs may include origination fees, processing charges, and potential prepayment penalties that can significantly impact the overall financial commitment.

Agricultural equipment financing approval requirements demand comprehensive financial documentation and rigorous assessment. Lenders typically examine multiple factors, including credit scores, business financial statements, tax returns, operational history, and projected revenue streams. Most financial institutions require a minimum credit score of 650, though specialized agricultural lenders might offer more nuanced evaluation processes that consider the unique challenges and seasonal nature of farming operations.

Review this quick summary of common hidden costs and approval requirements when pursuing equipment financing:

| Cost/Requirement | What to Expect | Potential Impact |

|---|---|---|

| Origination Fees | 1-3% of equipment price | Increases upfront expenses |

| Minimum Credit Score | Usually 650 or above | May limit access for some farms |

| Tax Documentation | 2-3 years required | Delays if records are incomplete |

| Down Payment | 10-25% of equipment value | Larger sum upfront |

| Maintenance Contracts | Sometimes required in leases | Adds to recurring costs |

Financing terms can vary dramatically, ranging from short-term agreements of 12 months to extended arrangements spanning 5-7 years. Farmers must carefully analyze loan duration, understanding that longer terms reduce monthly payments but increase total interest expenses. Some financing options include flexible provisions such as seasonal payment structures that align with harvest cycles, balloon payments, or equipment upgrade pathways that accommodate technological advancements and changing agricultural needs.

Pro Tip: Financial Preparedness Strategy: Create a comprehensive financial narrative before applying, including detailed projections of how the equipment will generate revenue, potential tax depreciation benefits, and a clear explanation of how the machinery fits into your broader agricultural business strategy.

Risks, Pitfalls, and Common Mistakes

Equipment financing presents numerous potential risks that farmers must carefully anticipate and navigate to protect their financial interests. Understanding these challenges is crucial for making informed decisions that prevent long-term economic complications and operational disruptions.

One of the most significant financial risks involves overestimating equipment productivity and underestimating total ownership costs. Farmers frequently miscalculate ongoing maintenance expenses, depreciation rates, and potential technological obsolescence. Hidden costs can include unexpected repair fees, insurance requirements, storage expenses, and potential downtime during equipment malfunctions. Many agricultural professionals fail to conduct comprehensive total cost of ownership analyses, leading to financial strain that extends far beyond the initial financing agreement.

Agricultural equipment financing strategies frequently expose farmers to complex contractual pitfalls that can compromise financial stability. Common mistakes include overlooking prepayment penalties, neglecting to negotiate flexible terms, and failing to thoroughly understand interest rate structures. Some financing agreements include restrictive clauses that limit equipment modification, mandate specific maintenance protocols, or impose severe penalties for early contract termination. Farmers must meticulously review every contractual detail, potentially consulting legal and financial professionals to fully comprehend the long-term implications of their financing commitments.

Technological and operational risks represent another critical dimension of equipment financing. Rapidly evolving agricultural technologies can render recently purchased machinery obsolete within short timeframes, creating significant economic challenges. Farmers must strategically assess equipment’s projected lifespan, potential upgrade pathways, and compatibility with emerging technological standards. Some financing arrangements offer more flexibility in equipment replacement or upgrading, while others lock farmers into rigid, potentially outdated equipment configurations.

Pro Tip: Risk Mitigation Strategy: Develop a comprehensive five-year equipment replacement and technological upgrade plan before finalizing any financing agreement, ensuring your machinery investment aligns with anticipated agricultural innovations and your specific operational requirements.

Enhance Your Farm Operations with Reliable Machinery Parts

Navigating the complexities of equipment financing requires careful planning and the right support for your agricultural machinery. The article highlights critical challenges like managing financing terms, maintenance costs, and ensuring your equipment remains up-to-date despite technological changes. At pexlivanidis.com, we understand these pain points and strive to provide you with over 20,000 high-quality tractor accessories and spare parts designed to keep your equipment running efficiently and reduce unexpected costs.

Whether you are upgrading your farm fleet with new machinery or maintaining existing equipment financed through loans or leasing programs staying ahead with dependable parts can make all the difference. Explore our extensive inventory and enjoy benefits such as free shipping in Greece on orders over 100€ and exclusive wholesale B2B memberships. Visit our homepage now to find the reliable parts you need. Equip your farm to thrive by acting today and securing the components that match your operational goals.

Discover solutions that empower your agricultural business by visiting Pexlivanidis tractor accessories and spare parts and take control over your equipment’s performance and longevity.

Frequently Asked Questions

What is equipment financing in agriculture?

Equipment financing in agriculture is a financial strategy that enables farmers to acquire necessary machinery and equipment, such as tractors and harvesters, without the need for large upfront payments. This can include loans, leasing options, and specialized credit lines that help manage cash flow while upgrading technology.

How do equipment loans and leasing differ?

Equipment loans allow farmers to borrow money to purchase equipment outright, resulting in full ownership after payment. In contrast, equipment leasing provides temporary use of machinery without ownership at the end of the lease term, which may be beneficial for equipment that could quickly become obsolete.

What factors should farmers consider when evaluating equipment financing options?

Farmers should consider interest rates, loan duration, down payment requirements, and the projected operational lifespan of the equipment. It’s vital to conduct a cost-benefit analysis to determine whether financing is more advantageous than outright purchase or rental.

What common risks are associated with equipment financing?

Common risks in equipment financing include overestimating the productivity of the equipment and underestimating total ownership costs, such as maintenance and insurance. Additionally, farmers may face contractual pitfalls and technological risks if equipment becomes obsolete too quickly or has strict terms that limit flexibility.